Recent announcements around the taxation of discretionary trusts have triggered a wave of questions from investors, particularly around whether to restructure into companies or alternative vehicles. The short answer at this stage is simple: first speak to your adviser about your personal circumstances, but generally for many people the answer will be, do not rush to restructure.

Below is a practical, investor-focused breakdown of what we know, what still matters, and where caution is required.

Implementation is still years away

The proposed changes are not expected to take effect until the financial year beginning 1 July 2028.

Importantly:

- Key mechanics are still subject to consultation and not legislated

- Areas like collection mechanics, franking credits and rollover relief remain unresolved

- The Government has proposed expanded rollover relief to restructure from 1 July 2027 for three years, but details are not final

- There may be a need for state government rollover relief if there are any stamp duty issues.

Acting now based on incomplete rules could trigger unnecessary CGT, stamp duty or restructuring costs that may not be needed.

What impact will there be for unit trusts?

For investors using unit trusts, including private unit trust structures, it appears there is no change proposed, if they meet the definition of a fixed trust.

- No proposed additional withholding obligations

- No minimum 30% tax applied to distributions

- No structural disadvantage relative to current settings

Assuming the law is passed on this basis, it’s likely Westbridge’s funds do not have any additional withholding obligations or minimum 30% tax rate on distributions. As such, unit trusts remain stable under the current proposals and are unlikely to require changes based on what is known today.

How will the minimum 30% withholding on discretionary trusts work?

It’s important to understand that the 30% withholding is on taxable income and not gross income.

For capital gains tax purposes, it is after the 50% discount and indexation.

To illustrate how this works, consider a trust that realises a capital in a year. The total gain is $1 million dollars. The asset was purchased on 1 July 2017 and sold on 1 July 2030. Assume that $800,000 of the gain eligible for the 50% CGT discount, resulting in $400,000 of taxable income. The second is a $200,000 gain where indexation is applied, reducing the taxable component to $150,000. In total, the trust would have $550,000 of taxable income from these transactions.

Under the proposed rules, the 30% minimum tax would be applied to this $550,000 taxable amount, resulting in a minimum tax (or withholding) of $165,000. In other words, the tax is calculated after the CGT discount and indexation adjustments, not on the original capital gains. The total withheld of the $1 million gain is 16.5%.

Do discretionary trusts still make sense?

Despite the headlines, discretionary trusts retain value in several scenarios.

A discretionary trust still makes sense where the main reasons are:

- Asset protection and family control

Trusts remain useful where assets or business interests should be separated from individuals, subject to the usual limits: personal guarantees, family law, bankruptcy clawbacks, director duties. - Succession planning

A trust can allow control to pass without transferring each underlying asset personally. - Beneficiaries are already taxed at 30% or more

If distributions are already going to adult beneficiaries whose marginal tax rate is 30% or higher, the proposed minimum tax may not increase overall tax. - Business flexibility still matters

For some private businesses, a trust can still be valuable for allocating income among genuinely involved family members, streaming certain classes of income where permitted, and managing succession.

Where discretionary trusts will not be as useful

They are much less compelling where the main purpose is:

- Distributing to low-income adults

The proposed 30% floor removes much of the benefit of distributing to adult children, low-income spouses or retirees where their actual marginal tax rate is below 30%. The credit is non-refundable, so the excess credit is wasted. - Using corporate beneficiaries

This is the most exposed area. Under the announced design, corporate beneficiaries do not get the non-refundable credit for trustee tax, and trustees receiving franked dividends must use franking credits to pay the minimum tax. That could make bucket-company arrangements unattractive or even punitive depending on final legislation. - Negatively geared property

Discretionary trusts have never been ideal for negatively geared investments because trust losses generally get trapped in the trust. However, if you had positive income from another trust, you could distribute income to the loss-making trust to utilise those losses. With the proposed changes and a minimum 30% withholding that is not refundable, it may not make sense to transfer income from one discretionary trust to another to use the losses.

Keep in mind that the key mechanics are still to be finalised after consultation, including collection mechanics, franking credit treatment and rollover relief details. Expanded rollover relief is proposed for three years from 1 July 2027 to help restructure out of discretionary trusts into companies or fixed trusts.

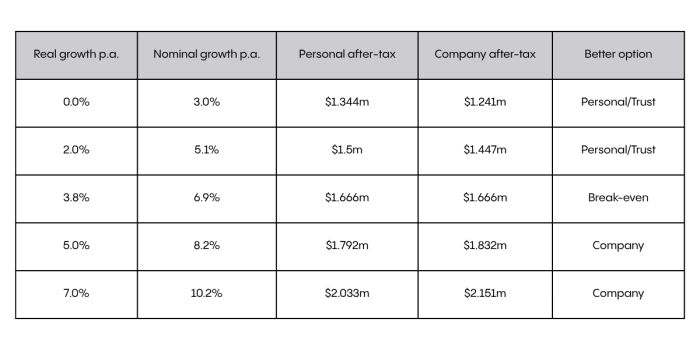

Will CGT be higher in a company or trust?

In short, it depends on key variables including the growth rate and the marginal tax rate. When it was 50% discount it was an easier decision – trusts usually fared better than a company.

Under the new regime, the minimum CGT of 30% is after indexation, so a trust will usually be better on most moderate growth assets as it benefits from indexation, whereas a company pays 30% CGT with no indexation. The possible exception is where it’s a high growth asset and the only likely beneficiaries are in the top marginal tax brackets, so a significant amount of the gain may be subject to 47% CGT.

A company tends to make sense if you have money there already, or it’s a multi-generational investment, where you are paying the higher marginal tax rates already and you don’t need the money.

It’s going to depend on each person’s circumstances and the expected gain, which of course is not possible to lock in the beginning of an investment.

Depending on the growth rate, one structure may be better than the other. This is illustrated by the below example on a $1 million investment over ten years and assuming 3% per annum inflation and a 47% marginal tax rate.

Of course, if it’s an income producing asset you need to consider the tax rates on the income through the period of the investment, not just the capital gains tax.

Note: If profits are later distributed out of a company, additional personal tax applies (offset by franking credits), which can erode the apparent benefit.

In Summary

- The most important point is that there is no urgency to act. Changes are not proposed to take effect until the financial year beginning 1 July 2028. Acting early could create unnecessary tax consequences.

- The smarter move is to wait for final legislation and model outcomes carefully before making any structural decisions.

- Talk to your advisers to determine the best strategy for you.

This article is general information only and does not constitute tax, legal or financial advice. You should obtain advice specific to your circumstances before acting.