Following the Federal Government’s proposed capital gains tax changes, investors are wondering which assets are more likely to provide a better risk adjusted return after tax.

The proposed CGT reforms are significant because they change the way investors are rewarded for capital growth. Under the current rules, investors who hold an asset for more than 12 months may generally be eligible for a 50% CGT discount. Under the proposed regime, that discount would be replaced by cost base indexation, meaning the asset’s cost base is adjusted for CPI and tax is applied only to the real gain above inflation. A 30% minimum tax rate (after indexation) would also apply to net capital gains calculated under the new method, but it could be as high as 47%.

The proposed system is more focused on taxing gains above inflation than the current system of a 50% discount. That distinction matters. An asset that delivers a steady income return and grows moderately above CPI may be less disadvantaged than a strategy whose return depends heavily on manufacturing a large capital gain.

This is one reason we believe the proposed changes may favour lower risk, income producing assets over higher risk value add strategies. A value-add fund typically takes on leasing, development, repositioning or timing risk with the aim of creating significant capital uplift. If successful, that uplift is likely to be a real gain above CPI, and under the proposed rules, it may be more fully taxed than under the current 50% discount regime.

Let’s look at two assets and see how the returns work. Assume the investment is $1 million for five years and returns were reinvested.

- Asset 1 is a steady income and growth asset targeting 12% per annum returns. This asset produces 7% per annum distributions and a target 5% per annum capital growth.

- Asset 2 is a value-add opportunity targeting 15% per annum, made up of 4% yield and 11% per annum capital growth.

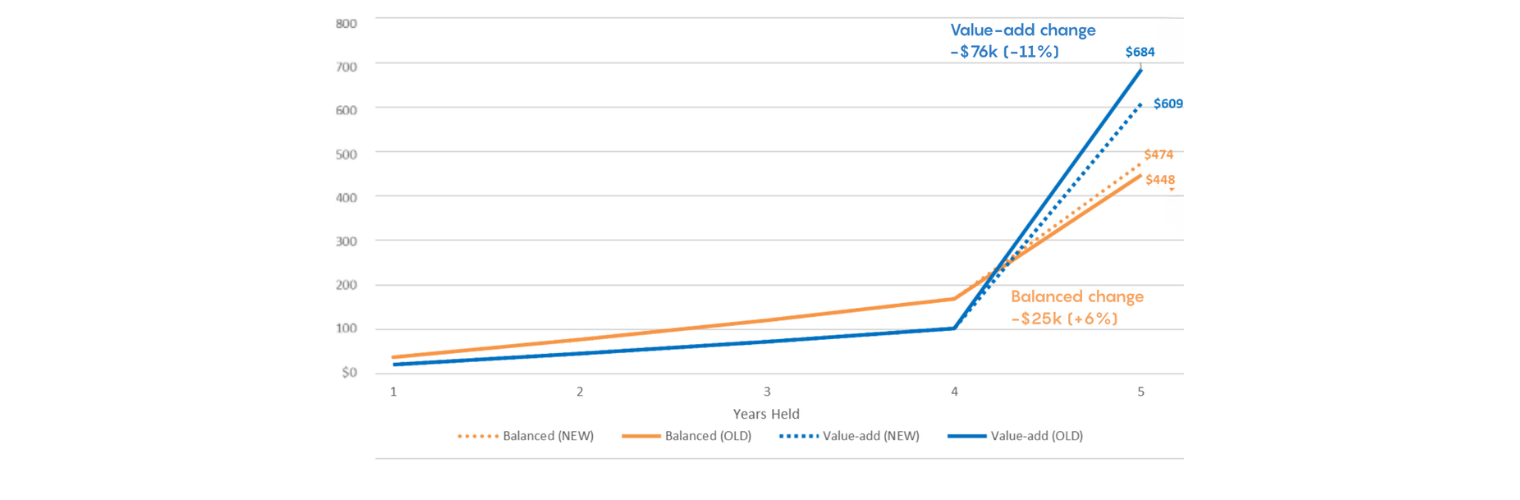

Assuming the top marginal tax rate and 3.5% inflation, the steady income and growth asset produces higher after-tax returns for the entire period until the sale.

The value-add asset does produce higher overall returns, but it is reliant on an exit price much higher than the purchase price. With the higher CGT under the new proposed system and an exit price that’s definitely not guaranteed, it’s worth asking whether the after-tax returns are worth the risk.

Accumulated After Tax Profit

(Old v New CGT Regime)

By contrast, a more stable commercial property investment with a quality tenant and regular rental income has a different return profile. The strategy is not relying solely on a large capital gain at exit. A meaningful component of the return is expected to come from income distributions over the hold period. To the extent the asset also grows in value over time, CPI indexation may help ensure that inflationary growth is not taxed as a real gain.

That is particularly relevant in the current environment. Higher interest rates have increased the cost of capital and placed greater scrutiny on asset quality, tenant covenant and income durability. Geopolitical uncertainty has also reinforced the importance of defensive investment characteristics. In this context, we believe investors may increasingly value assets that offer stable income, strong tenant fundamentals and a clear long term property rationale.

Of course, tax outcomes will vary by investor, structure and personal circumstances, and the proposed CGT changes remain subject to legislation. Investors should obtain their own tax advice before making any investment decision.

However, at a portfolio level, we believe the direction of travel is clear: if the proposed CGT changes proceed, investors outside of superannuation funds may place greater value on assets that deliver income along the way, rather than strategies that rely predominantly on larger capital gains at exit.

To note:

While the outcome will depend on your investment vehicle there’s a few key points to keep in mind:

- The proposed CGT changes are not yet law, but the Government has announced that from 1 July 2027 the 50% CGT discount would be replaced with CPI cost-base indexation and a 30% minimum tax rate (after indexation) on capital gains for individuals, trusts, and partnerships. Ultimately the capital gains tax could be as high as 47% on the amount above indexation.

- This shifts the relative tax benefit away from high capital growth strategies and towards assets where returns are more weighted to stable recurring income and reasonable real capital growth.

- Lower risk, stable property assets may be better aligned with the new regime because CPI indexation reduces the taxable component of inflation driven growth, while rental income remains a key part of total return.

- Value-add or higher risk funds may be more exposed to the change, because their investment thesis often relies on creating larger capital gains above CPI. These gains that may no longer receive the 50% CGT discount.

- The Westbridge Moorabbin Property Fund is designed around defensive income, with an institutional grade industrial asset, a blue-chip tenant in Amcor, and future infill redevelopment potential.