At Westbridge, we believe transparency in how we calculate unit prices is fundamental to maintaining investor confidence. This note is a simplified explanation of our unit pricing approach and explains, in practical terms, how units in our funds are priced and why unit prices may move over time.

Step 1: Work out the Net Asset Value

The core principle underpinning our unit pricing is the Net Asset Value (NAV) of the Fund.

Put simply, the NAV is defined in the fund constitution and represents the total value of the fund’s assets, less its liabilities. This is based off the financial statements prepared monthly by our in-house accounting team and includes:

- The value of the underlying property assets;

- Cash and other assets held by the fund; and

- Any liabilities such as debt and creditors.

The valuation of property assets is undertaken in accordance with our valuation policy and consistent with industry practice, including independent valuations at minimum intervals for commercial property funds.

Step 2: Adjust for Acquisition Costs

When a fund buys a property there are upfront costs including stamp duty, legal fees, and due diligence costs. Rather than expensing these all at once, these costs are added back to the fund’s NAV and then amortised over the expected term of the fund.

This approach ensures that the cost of acquiring the asset is shared equitably across all investors over time. Without this adjustment, incoming investors could effectively “buy in” after these costs have been incurred without contributing to them, which would unfairly disadvantage existing unitholders.

Step 3: Divide by Units on Issue

Once we have the adjusted NAV, we divide it by the total number of units in the fund:

Unit Price = Adjusted NAV ÷ Units on Issue

It’s simple in principle, but the movements in NAV are what most investors have questions about.

Commercial Property Funds: What to Expect

In a commercial property fund that holds income-generating assets unit price movements are generally predictable.

In most cases, a reduction in the unit price over a 6–12-month period may occur as the acquisition costs are amortised and the property has not yet been revalued. This does not necessarily mean that the investment is performing below expectation.

Over the medium to long term, value is delivered through two sources:

- Income: regular distributions from rental revenue

- Capital growth: as the property assets are revalued over time, that uplift flows through to the unit price. This can also mean that the unit price can move suddenly as the valuations are reflected in the NAV.

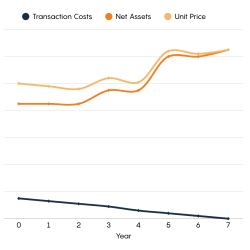

Example for illustration purposes:

Unit Price Movements*

Development Funds: What to Expect

For funds that include development or value-add projects, unit price movements can differ from passive income funds.

- During development & construction

During the construction or development phase, costs are being incurred (construction, finance, professional fees) while the asset is not yet generating income. As a result, unit prices will decline during this period, reflecting the accumulation of costs before value is fully realised, with allowance for risk included in some cases. - Nearing practical completion

As a project nears completion the remaining development risk often reduces as final costs and expected sales prices become clearer. This can still result in a softening or stabilisation in the unit price, even though the project is progressing successfully. - At or following completion

For accounting purposes, the completed development is classified as inventory under Australian Accounting Standards, and as such must be recorded at cost when calculating the NAV. However, for unit pricing purposes an adjustment can be made to take into account the market value of the completed development, which may be above total development cost.

This can result in an uplift in unit price, as the embedded development margin is realised.

The Bottom Line

Unit price movements, particularly in development strategies, are best understood over the full lifecycle of an investment, not quarter to quarter or even year to year. Short-term dips are often a normal and expected part of how property funds work.

The goal in all our funds is to deliver strong risk-adjusted returns through both income and capital growth over time.

If you have any questions about how your fund is priced, please don’t hesitate to give our team a call, we’re always happy to talk it through.

*This information has been prepared by Westbridge Funds Management as a general guide only. Westbridge Funds Management and its related entities do not make any representations or give any warranties that the information contained within is or will remain accurate or complete at all times and they disclaim all liability for harm, loss, costs, or damage which arises in connection with the use or reliance on the information. Westbridge Funds Pty Ltd ABN 33 652 852 214 AFSL 533936. Westbridge Asset Management Pty Ltd ABN 48 151 957 676. Westbridge Property Securities Ltd ABN 28 091 623 862. AFS Licence 238386. Momentum Wealth Projects Pty Ltd ABN 29 090 792 439 t/a Westbridge Urban.